What Is Social Security Disability Insurance (SSDI)? The Definitive Plain-Language Guide To SSDI and SSI

Social Security Disability Insurance (SSDI) is a federal program that provides monthly financial benefits to people who can no longer work because of a serious medical condition or disability. The program is designed to help individuals who have worked and paid into the Social Security system but are now unable to earn a living due to a long-term illness or injury.

SSDI is administered by the Social Security Administration (SSA) and funded through payroll taxes collected under the Federal Insurance Contributions Act (FICA). As you work, you earn work credits by paying Social Security taxes. These credits help determine whether you qualify for SSDI benefits if you become disabled. In general, you must have worked long enough and recently enough in jobs covered by Social Security to be eligible.

To qualify for SSDI, you must meet the SSA's definition of disability. The program does not provide benefits for temporary or partial disabilities. Instead, your medical condition must prevent you from performing the work you did previously and keep you from adjusting to other types of substantial work. Your disability must also have lasted, or be expected to last, at least 12 months or be expected to result in death.

If you meet both the work history requirements and the SSA's medical criteria, you may qualify to receive monthly disability benefits. Because every application is evaluated individually, the SSA reviews both your medical records and your employment history when determining eligibility.

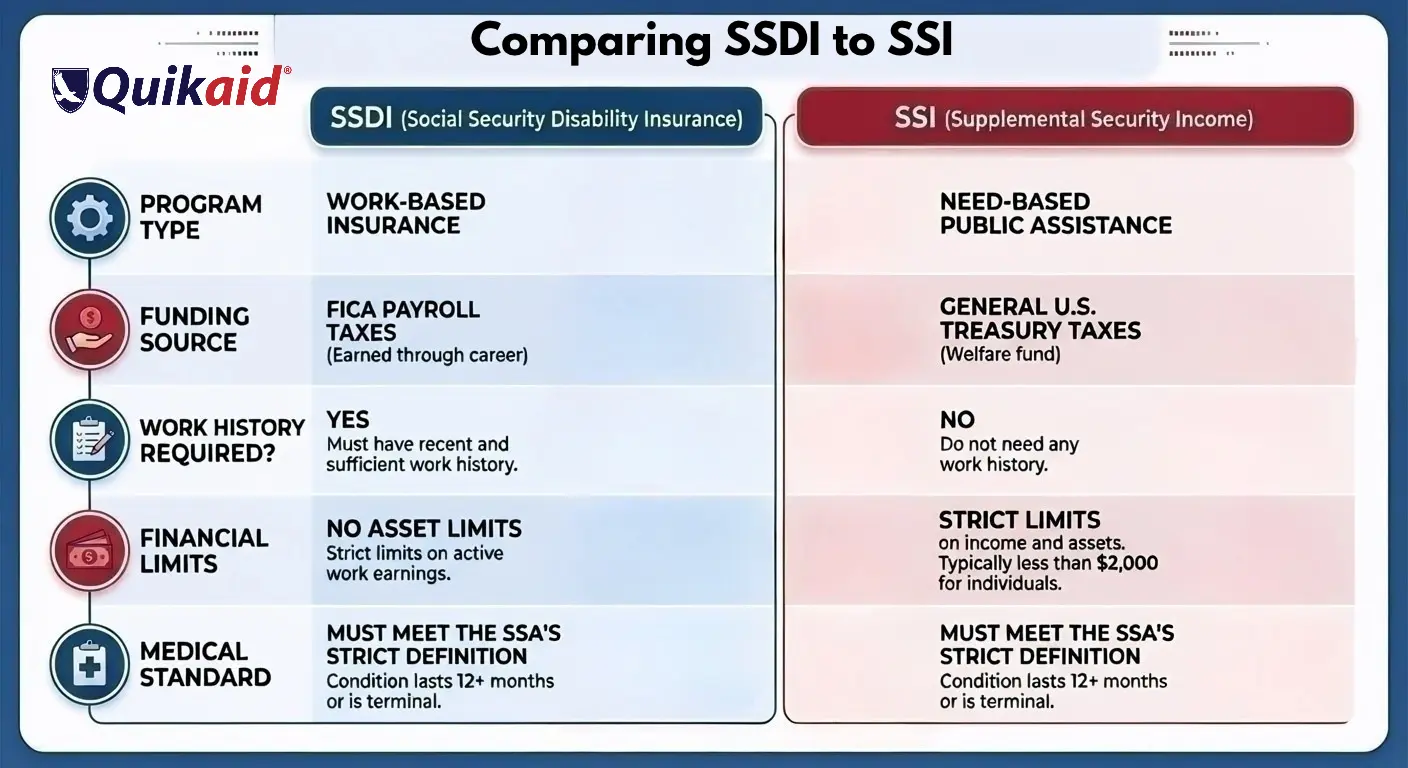

SSDI vs. SSI — What's the Difference?

Although Social Security Disability Insurance (SSDI) and Supplemental Security Income (SSI) are both part of America’s disability insurance program and they are both administered by the Social Security Administration (SSA) and provide benefits to people with qualifying disabilities, they are separate programs with different eligibility requirements.

One important similarity is that both programs use the same medical definition of disability. This means applicants must meet the same medical criteria regardless of which program they are applying for.

The main differences between SSDI and SSI involve work history and financial eligibility. SSDI is based on a person's work record and the Social Security taxes they have paid through employment. SSI, on the other hand, is a needs-based program for individuals with limited income and resources, regardless of their work history. Understanding these differences can help determine which program may be available based on your individual circumstances.

Understanding the Differences Between SSDI and SSI

Social Security Disability Insurance (SSDI) is available to individuals who have worked and paid Social Security taxes for a sufficient period of time. Eligibility is based on a person's work history, and the monthly benefit amount is generally determined by their lifetime earnings covered by Social Security.

Supplemental Security Income (SSI) is a separate program for individuals with disabilities who have limited income and resources. Unlike SSDI, SSI does not require a qualifying work history. Instead, eligibility is based on financial need, and the program provides benefits to eligible adults and children who meet the Social Security Administration's income, resource, and disability requirements.

In some situations, an individual may qualify to collect both SSDI and SSI. This is known as receiving concurrent benefits. Concurrent eligibility is most common when a person qualifies for SSDI based on their work history but receives a relatively low SSDI benefit and also meets SSI's financial eligibility requirements.

Because SSDI and SSI have different eligibility rules, benefit calculations, and health insurance provisions, understanding how each program works can help you determine which benefits you may qualify for based on your individual circumstances.

What Is SSDI (Social Security Disability Insurance)?

Social Security Disability Insurance (SSDI) is a federal program that provides monthly benefits to eligible individuals who are unable to work because of a qualifying long-term disability. The program is designed for workers who have paid Social Security taxes and have earned sufficient work credits through employment.

Unlike needs-based programs, eligibility for SSDI is based primarily on your work history and whether you meet the Social Security Administration's (SSA) medical definition of disability.

How SSDI Is Funded

SSDI is funded through payroll taxes collected under the Federal Insurance Contributions Act (FICA). These taxes are paid by workers, employers, and many self-employed individuals. The money is deposited into the Social Security trust funds, which finance retirement, survivor, and disability benefits.

Because SSDI is funded through payroll taxes, applicants generally must have worked in jobs covered by Social Security to qualify for benefits.

Work Credits and Eligibility

To receive SSDI benefits, you must have earned enough work credits before becoming disabled. Work credits are based on your annual wages or self-employment income, and the amount of earnings required to earn a credit is adjusted each year.

Most people can earn up to four work credits per year. In general, adults who become disabled typically need 40 work credits, with 20 earned during the 10 years immediately before their disability began. However, younger workers may qualify with fewer credits because they have had less time to build a work history.

Meeting the work credit requirement alone does not guarantee eligibility. Applicants must also satisfy the SSA's medical requirements for disability.

Medicare Eligibility

People who qualify for SSDI may also become eligible for Medicare, the federal health insurance program. Medicare coverage can help pay for hospital care, physician services, and other covered medical expenses.

In most cases, Medicare coverage begins 24 months after a person becomes entitled to SSDI benefits. During this waiting period, individuals may need to obtain health insurance through another source, such as an employer-sponsored plan, a spouse's health plan, COBRA, the Health Insurance Marketplace, or Medicaid, if they qualify.

There are important exceptions to the 24-month waiting period. Individuals who qualify for SSDI because of Amyotrophic Lateral Sclerosis (ALS) generally become eligible for Medicare as soon as their SSDI benefits begin. People with End-Stage Renal Disease (ESRD) may also qualify for earlier Medicare coverage if they meet the program's eligibility requirements.

What Is SSI (Supplemental Security Income)?

Supplemental Security Income (SSI) is a federal program that provides monthly financial assistance to eligible adults and children with disabilities, as well as adults age 65 and older who have limited income and resources. The program is designed to help individuals meet basic living expenses, such as food, clothing, and shelter.

Unlike Social Security Disability Insurance (SSDI), SSI is a needs-based program. Eligibility is determined by an individual's financial circumstances rather than their work history.

No Work History Is Required

SSI is funded through general federal tax revenues rather than Social Security payroll taxes. Because of this, you do not need to have worked or paid Social Security taxes to qualify.

Instead, eligibility is based on two primary factors:

- Whether you meet the Social Security Administration's (SSA) medical definition of disability (or are age 65 or older), and

- Whether your income and financial resources fall within the program's limits.

Income and Resource Limits

To qualify for SSI, applicants must meet the SSA's financial eligibility requirements. The agency reviews both the income you receive and the resources you own because assets affect SSI eligibility.

Resources include assets such as cash, bank accounts, investments, and certain property. Some assets are excluded from the resource calculation, including the home you live in and, in most cases, one vehicle used for transportation.

For 2026, the federal resource limits are:

- $2,000 for an individual

- $3,000 for a married couple

The SSA also evaluates countable income, which may include wages, pensions, Social Security benefits, and certain types of financial support. The amount of countable income you receive can affect both your eligibility and your monthly SSI payment.

Federal SSI Benefit Amounts for 2026

If you qualify for SSI and have no countable income, you may receive the maximum federal monthly benefit. For 2026, the maximum federal benefit rates are:

- Individual: $994 per month

- Eligible couple: $1,491 per month

If you have countable income, your monthly SSI payment is generally reduced according to SSA rules on how SSI benefit amounts are determined. In addition to the federal benefit, some states provide an optional state supplement that increases the monthly payment for eligible recipients.

Medicaid Eligibility

In many states, people who qualify for SSI also become eligible for Medicaid, which helps cover healthcare costs such as doctor visits, hospital care, and prescription medications.

In most states, Medicaid eligibility begins when SSI benefits start, although some states use different eligibility rules or require a separate application to qualify for Medicaid. Because these policies vary, applicants should check the Medicaid requirements in their state to determine how coverage is provided.

Who Qualifies for Social Security Disability Benefits?

Qualifying for Social Security disability benefits involves more than having a medical diagnosis or a statement from your doctor. The Social Security Administration (SSA) follows a standardized evaluation process to determine whether an applicant meets the program's legal definition of disability.

When reviewing an application, the SSA considers several factors, including your current work activity, the expected duration of your medical condition, your work history (for SSDI), and your ability to perform work.

1. Current Work Activity (Substantial Gainful Activity)

The SSA first evaluates whether you are currently working and earning more than a certain monthly amount. This is known as Substantial Gainful Activity (SGA).

For 2026, the monthly SGA earnings limits are:

- $1,690 for most individuals

- $2,830 for individuals who meet the SSA's definition of statutory blindness

In general, working affects your SSDI or SSI eligibility. If your earnings are above the applicable SGA limit, you will not be considered disabled under SSA rules. These limits apply to earned income from work rather than income from investments or other non-work sources.

2. Duration of the Medical Condition

Social Security disability benefits are intended for long-term disabilities. To qualify, your medical condition must:

- Have lasted, or be expected to last, at least 12 consecutive months, or

- Be expected to result in death.

Conditions that are expected to improve within a shorter period generally do not meet the SSA's duration requirement.

3. Work History Requirements for SSDI

Applicants seeking Social Security Disability Insurance (SSDI) must also meet work history requirements. Eligibility is based on the number of work credits earned through employment covered by Social Security.

Most adults who become disabled need approximately 40 work credits, with 20 credits earned during the 10 years immediately before the disability began. Younger workers may qualify with fewer credits depending on their age.

These work credit requirements apply only to SSDI. Individuals who do not qualify for SSDI based on their work history may still be eligible for Supplemental Security Income (SSI) if they meet the program's financial and medical requirements.

4. The SSA's Five-Step Disability Evaluation

If an applicant meets the initial non-medical requirements, the SSA uses a five-step evaluation process to determine whether they qualify for disability benefits.

- Are you working at the Substantial Gainful Activity (SGA) level?

- Is your medical condition considered severe enough to significantly limit your ability to perform basic work activities?

- Does your condition meet or medically equal one of the impairments listed in the SSA's Listing of Impairments (often called the "Blue Book")?

- Can you perform any of your past relevant work despite your medical condition?

- Considering your age, education, work experience, and functional limitations, can you adjust to other work that exists in significant numbers in the national economy?

The SSA reviews each step in order and makes a decision based on the evidence available. A finding that an applicant can perform past work or adjust to other work may result in a denial of benefits. Conversely, applicants who meet the applicable requirements and satisfy the SSA's disability criteria may be approved for benefits.

The SSA's Definition of Disability

When most people think of being "disabled," they think of it in casual terms—having a major injury, being unable to do certain physical tasks, or receiving a diagnosis from a doctor. However, the Social Security Administration (SSA) operates on a completely different wavelength.

The SSA enforces one of the strictest, most rigid definitions of disability in the entire world. It is a legal and regulatory standard that goes far beyond a simple doctor's note.

The Two Core Pillars of the SSA Definition

To be legally considered disabled by the federal government, you must meet a two-pronged test that evaluates both your current ability to work and your medical timeline:

- The Work Test (Inability to Do Substantial Work): You must be completely unable to engage in what the SSA calls Substantial Gainful Activity (SGA). This means your physical or mental impairments must be so severe that you cannot perform your past jobs, and you cannot adjust to any other type of sustainable, profitable work anywhere in the national economy.

- The Duration Test (The 12-Month Rule): Your medical condition cannot be temporary. The SSA explicitly states that your impairment must have lasted, or be expected to last, for a continuous period of at least 12 months, or be expected to result in death.

An All-or-Nothing System: No Partial Disability

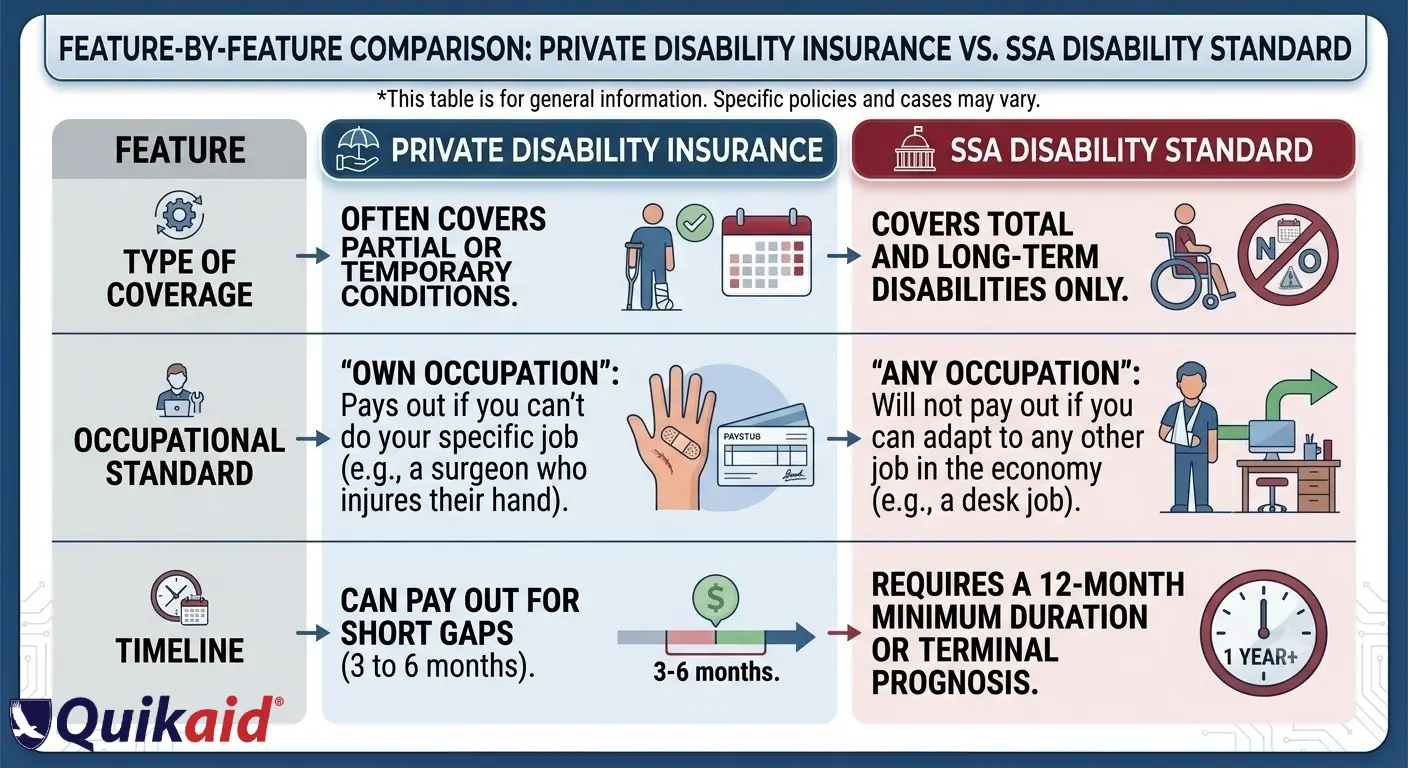

This is the part that catches most applicants off guard: the SSA does not pay for partial or short-term disability.

Many state programs or private insurance policies use a percentage-based system—for example, classifying you as "20% disabled" or "partially disabled" if you can only work part-time or can no longer lift heavy objects. The SSA does not do this. Under their rules, you are either 100% disabled and completely incapable of sustaining a living, or you are not disabled at all. There are no short-term Social Security disability benefits.

SSA vs. Private Disability Insurance Definitions

If you have ever dealt with a private long-term disability (LTD) policy through an employer, you might assume the government's process is similar. In reality, private insurance and the SSA use fundamentally different standards.

Because the SSA looks at your ability to do any job rather than just your past job, winning a government disability claim requires a much higher burden of medical proof than most private insurance claims.

Work Credits and SSDI Eligibility

To qualify for Social Security Disability Insurance (SSDI), applicants must generally have a sufficient work history in jobs covered by Social Security. The Social Security Administration (SSA) uses a system of work credits to determine whether an individual has worked long enough and recently enough to be eligible for benefits.

Meeting the work credit requirement is one part of the eligibility process. Applicants must also meet the SSA's medical definition of disability.

How Work Credits Are Earned

Work credits are earned through employment or self-employment in which Social Security taxes are paid. The number of credits you earn depends on your annual earnings, up to a maximum allowed each year.

For 2026:

- You earn one work credit for every $1,890 in covered earnings.

- You can earn up to four work credits per year.

- Once you earn $7,560 during the year, you have earned the maximum four credits for that year.

Earning income above the annual maximum does not increase the number of work credits you receive.

Work Credit Requirements for Most Adults

For many applicants who become disabled at age 31 or older, the SSA generally applies two work credit requirements:

- Lifetime work requirement: You typically need 40 total work credits, which is generally equivalent to about 10 years of work.

- Recent work requirement: At least 20 of those credits usually must have been earned during the 10 years immediately before your disability began.

These requirements help ensure that applicants have both an established work history and recent participation in the workforce. Individuals who have not worked in covered employment for an extended period may no longer meet the recent work requirement, even if they earned enough credits earlier in their careers.

Special Rules for Younger Workers

Because younger workers have had less time to earn work credits, the SSA uses different eligibility rules for people who become disabled at a younger age.

- Before age 24: Applicants generally need 6 work credits earned during the three-year period before their disability began.

- Ages 24 through 30: Applicants generally need work credits for about half of the time between age 21 and the date their disability began. For example, someone who becomes disabled at age 27 would generally need credits representing about three years of work.

- Age 31 and older: The standard work credit requirements generally apply.

The number of work credits required can vary depending on a person's age and the date their disability began. The SSA reviews each application individually to determine whether the applicable work credit requirements have been met.

Medical Conditions That May Qualify

A question people often ask is whether a particular medical condition automatically qualifies them for Social Security disability benefits. In most cases, the answer is no.

While the Social Security Administration (SSA) recognizes many medical conditions that may qualify for disability benefits, a diagnosis alone is not enough to receive approval. The SSA evaluates how a medical condition affects a person's ability to perform work-related activities rather than relying solely on the name of the diagnosis.

The SSA's Listing of Impairments ("Blue Book")

The SSA uses a medical reference called the Listing of Impairments, often referred to as the Blue Book, when evaluating disability claims. The Blue Book describes medical conditions and the evidence needed to meet the SSA's disability standards.

The listings are organized into major body systems, including:

- Musculoskeletal disorders

- Cardiovascular disorders

- Neurological disorders

- Mental disorders

- Respiratory disorders

- Immune system disorders

- Cancer (malignant neoplastic diseases)

- Digestive, endocrine, kidney, skin, and other body system disorders

Each listing includes specific medical criteria that must be documented through medical records, laboratory findings, imaging studies, or other objective evidence. Applicants whose conditions meet or medically equal a listed impairment may qualify for benefits if they also satisfy the applicable non-medical eligibility requirements.

How the SSA Evaluates Medical Evidence

Many applicants do not have a condition that exactly matches one of the types of medical evidence the SSA requires. In those cases, the SSA evaluates the overall impact of the condition on the person's ability to work.

When reviewing a claim, the SSA considers medical evidence such as:

- Physician and specialist treatment records

- Diagnostic tests, including MRI scans, X-rays, CT scans, and laboratory results

- Hospital and clinic records

- Prescription history and ongoing treatment

- Information about physical and mental limitations

The SSA also evaluates how a medical condition affects everyday work-related activities, including the ability to sit, stand, walk, lift, carry, concentrate, remember instructions, interact with others, and maintain a regular work schedule.

Conditions That Are Not Specifically Listed

Some medical conditions are not listed individually in the Blue Book. Even so, an applicant may still qualify for disability benefits if the medical evidence shows that the condition is severe enough to prevent substantial work activity.

The SSA reviews each application individually, considering the combined effects of all medically determinable impairments, the available medical evidence, and the applicant's functional limitations when making a disability determination.

How Much Does Social Security Disability Pay?

The Social Security Administration (SSA) administers two separate disability programs: Social Security Disability Insurance (SSDI) and Supplemental Security Income (SSI). Each program calculates monthly payments differently, so the amount a beneficiary receives depends on which program they qualify for.

How SSDI Payments Are Calculated

SSDI is an insurance-based program. Monthly payment amounts are determined by a recipient's earnings history, not by the severity of their medical condition or their financial need.

The SSA calculates SSDI benefits using a two-step formula:

Average Indexed Monthly Earnings (AIME): The SSA reviews a worker's earnings record and selects up to 35 of their highest-earning years. These past wages are indexed to account for national wage growth over time, then averaged to produce a baseline monthly earnings figure.

Primary Insurance Amount (PIA): A progressive percentage formula is then applied to the AIME. The Primary Insurance Amount (PIA) formula replaces a higher percentage of lifetime income for lower-wage earners than for higher-wage earners.

2026 SSDI Payment Figures

- National average: The estimated average SSDI benefit for a single disabled worker is $1,630 per month. Most recipients receive between $1,580 and $1,810 per month, depending on their earnings history.

- Maximum benefit: The maximum possible SSDI payment is $4,152 per month. Reaching this amount requires earnings at or above the Social Security taxable wage cap for most of a working career, which few applicants achieve.

How SSI Payments Are Determined

SSI is a need-based program and does not consider past earnings. Instead, the federal government sets a flat maximum monthly benefit, known as the Federal Benefit Rate, that applies nationwide.

The 2026 maximum federal SSI payments are:

- Eligible individual: $994 per month

- Eligible married couple: $1,491 per month

These figures represent the maximum federal payment. The SSA reduces this amount based on any "countable income" a recipient has, including part-time wages, pensions, and in-kind support such as free housing provided by a family member. Countable income is subtracted from the maximum benefit, lowering the monthly payment accordingly.

Cost-of-Living Adjustments (COLA)

Both SSDI and SSI benefits are subject to an annual Cost-of-Living Adjustment (COLA), which is designed to preserve purchasing power as consumer prices rise.

Each fall, the SSA reviews inflation data based on the Consumer Price Index. If prices have increased, a percentage-based adjustment is applied to all disability benefits beginning the following January. The 2026 COLA increased monthly benefits by 2.8%.

This annual adjustment applies to both programs, ensuring that SSDI and SSI payments keep pace with changes in the cost of living.

How to Apply for Social Security Disability

The Social Security Administration (SSA) offers several methods for filing a disability claim under SSDI or SSI. Applicants can choose the filing method that works best for their circumstances, but all claims follow the same review process and documentation requirements.

Three Ways to File an Social Security Disability Application

Online: Applications can be submitted directly at ssa.gov. The online portal allows applicants to save their progress and complete the forms in multiple sessions. This is generally the fastest filing method.

By phone: Applicants can call the SSA's national toll-free line at 1-800-772-1213 to speak with a representative and schedule an appointment to complete the application by phone.

In person: Applications can be filed at a local Social Security field office. Walk-ins are accepted, but scheduling an appointment in advance is recommended to reduce wait times.

Documents Required to File a Claim

Gathering complete records before filing helps prevent administrative delays. Applicants should prepare the following:

Personal information: Social Security number, birth certificate, and proof of U.S. citizenship or lawful residency status.

Medical evidence: A complete list of treating doctors, hospitals, and clinics, including contact information and dates of visits. Applicants should also compile medical records, laboratory results, imaging reports (MRI, X-ray), and a list of all prescribed medications.

Work history: W-2 forms or self-employment tax returns from the previous year, along with a summary of the types of work performed over the past 15 years.

Financial records (SSI applicants only): Bank statements, vehicle titles, and documentation of any current income or financial resources.

Claim Timeline and Approval Rates by Stage

Disability claims move through distinct stages, and most applicants encounter the appeals process before receiving a decision in their favor. This has an impact on how long disability claims take.

1. Initial Application (3 to 6 months)

In the initial disability decision, The application is reviewed by an examiner at a state Disability Determination Services agency. According to Quikaid's historical data, approximately 67% of initial applications are denied. Roughly one-third of claimants are approved at this stage.

2. Reconsideration (an additional 3 to 6 months)

Applicants who are denied have 60 days to request Reconsideration, in which a different examiner reviews the file. Approval rates in the Reconsideration stage fall to approximately 13–15%, and most claims are denied a second time.

3. Administrative Law Judge (ALJ) Hearing (1 to 3+ years from initial filing)

Claims denied at Reconsideration can be appealed to a hearing before an Administrative Law Judge. This stage offers the highest statistical likelihood of approval, at roughly 50%. However, hearing wait times can extend from several months to years.

The Role of Professional Representation

Because SSA medical evidence standards are complex and initial denial rates are high, many applicants work with a professional representative. Errors such as a missed form or an omitted physician's statement can delay a claim by months or result in dismissal.

Experienced disability representatives are familiar with the medical documentation the SSA requires, can obtain missing medical records efficiently, and can prepare a claim for presentation before an Administrative Law Judge. Applicants who want assistance with their claim can request a free case evaluation from Quikaid.

What Happens After You Apply?

After a disability application is submitted online, by phone, or in person, the local Social Security office completes the non-medical portion of the review, verifying work history, financial assets, and other eligibility factors. The file is then transferred to a specialized state agency for the medical and vocational evaluation that determines the outcome of the claim.

Step 1: The Case Is Assigned to State DDS

The medical file is assigned to the applicant's state Disability Determination Services (DDS) office. DDS is a federally funded state agency staffed by trained disability examiners, medical consultants, and psychologists.

The assigned DDS examiner is responsible for gathering the evidence needed to make a determination. This includes:

- Requesting medical records, treatment histories, and lab results directly from the applicant's healthcare providers.

- Sending Activities of Daily Living (ADL) questionnaires to the applicant to document how the condition affects daily functioning.

- Scheduling a Consultative Examination (CE) with an independent physician, at government expense, if the existing medical records are outdated or missing critical test results.

Step 2: The 5-Step Sequential Evaluation Process

To keep decisions objective and consistent nationwide, the DDS examiner applies the SSA's mandatory 5-Step Sequential Evaluation Process. Each step is evaluated in order, and a claim can be approved or denied at specific checkpoints:

1. Substantial Gainful Activity (SGA): Is the applicant working and earning above the SGA limit of $1,690 per month? If yes, the claim is denied. If no, the evaluation continues.

2. Severity: Is the condition severe enough to limit basic work activities, and has it lasted (or is it expected to last) at least 12 months? If no, the claim is denied. If yes, the evaluation continues.

3. Medical Listings: Does the condition meet or medically equal a listing in the SSA's Listing of Impairments (the "Blue Book")? If yes, the claim is approved at this step. If no, the evaluation continues.

4. Past Relevant Work: Can the applicant still perform any of the jobs they held during the past 5 years? If yes, the claim is denied due to residual functional capacity (RFC). If no, the evaluation continues.

5. Adjustment to Other Work: Based on age, education, and transferable skills, can the applicant adjust to any other sustainable work in the national economy? If yes, the claim is denied. If no, the claim is approved.

Step 3: The Initial Decision

After weighing all medical and vocational evidence, DDS issues one of two outcomes:

- Approved: Claims are approved when the applicant meets a medical listing at Step 3 or is found unable to perform any work at Step 5. The file returns to the local Social Security office, which finalizes the monthly benefit amount and establishes the healthcare coverage start date.

- Denied: If the examiner determines the applicant can still perform past work or adjust to other employment, the claim is denied and a formal denial letter is mailed to the applicant.

Step 4: The Right to Appeal

A denial does not end the claim. Roughly 67% of initial applications are denied, and the SSA provides a multi-tiered appeals process. Applicants have 60 days from the date on the denial letter to file an appeal at each level:

- Reconsideration: A different DDS examiner conducts a full review of the file, including any new medical evidence submitted. Most reconsideration requests result in a second denial.

- Administrative Law Judge (ALJ) Hearing: If the claim is denied at Reconsideration, the applicant can request a live hearing before an independent judge. This stage offers the highest likelihood of approval; the applicant and their representative can present testimony, clarify medical records, and question vocational experts directly.

- Appeals Council: If the ALJ denies the claim, the applicant can request review by the national Appeals Council in Falls Church, Virginia. The Council reviews the case strictly for legal or procedural errors by the judge. It can approve benefits, deny the request, or remand the case for a new hearing.

Social Security Disability Benefits: Frequently Asked Questions

The Social Security Administration's rules, terminology, and processing timelines raise common questions for applicants. The answers below address the questions most frequently asked when filing for disability benefits.

Can an applicant work part-time while applying for or receiving disability benefits?

Yes. Part-time work is permitted, but gross monthly earnings must remain below the SSA's Substantial Gainful Activity (SGA) threshold. For 2026, the SGA limit is $1,690 per month for non-blind individuals and $2,830 per month for statutorily blind individuals. Earnings above these limits result in denial of a pending application or termination of active benefits.

How long does it take to get a decision on a disability claim?

The timeline depends on whether the claim is approved initially or requires an appeal. An initial decision from state Disability Determination Services (DDS) typically takes 3 to 6 months. Because roughly 67% of initial applications are denied, most claimants proceed through the appeals process. Claims that reach an Administrative Law Judge hearing can take 1 to 3+ years in total from the initial filing.

What is the primary difference between SSDI and SSI?

The programs differ in how eligibility is established. SSDI is an insurance program funded by FICA payroll taxes and requires a sufficient, recent work history. SSI is a need-based program with no work history requirement, but it imposes strict asset limits (less than $2,000 for an individual) and income caps. Both programs use the same medical definition of disability.

How much are monthly disability payments?

Payment amounts depend on the program. For 2026, the maximum federal SSI benefit rate is $994 per month for an individual and $1,491 per month for a couple. SSDI payments are calculated from the recipient's lifetime earnings history using the SSA's benefit formula, with most disabled workers receiving between $1,580 and $1,810 per month.

Do disability benefits expire after a certain period?

Disability benefits have no built-in expiration date, but they are not guaranteed for life. The SSA periodically reviews each recipient's medical file through a Continuing Disability Review (CDR) to determine whether the condition has improved. If medical evidence shows significant improvement and an ability to return to work, benefits end. Otherwise, disability benefits automatically convert to standard retirement benefits when the recipient reaches full retirement age.

What should an applicant do if the initial application is denied?

A denied applicant should file an appeal rather than a new application; starting over restarts the process and forfeits the original filing date. Applicants have 60 days from the date on the denial letter to file a Request for Reconsideration. If Reconsideration is denied, there is an additional 60-day window to request a hearing before an Administrative Law Judge, the stage that historically yields the highest approval rates.

The Bottom Line

SSDI and SSI are governed by rigid legal standards, extensive documentation requirements, and initial approval rates of roughly one in three. For most applicants, that means confronting denials, strict deadlines, and an appeals process that can extend for years — often while managing a serious health condition at the same time. Applicants are not required to navigate this system alone, and the data suggests most shouldn't. This is why it matters how disability representatives charge for their services.

Since 1993, Quikaid has helped thousands of Americans secure the disability benefits they qualified for. Quikaid's team manages the components of a claim where errors most often cause delays or denials: gathering complete medical evidence, meeting every filing deadline, and preparing cases for each stage of review, including Administrative Law Judge hearings. This allows claimants to direct their energy toward their health rather than the paperwork.

Quikaid offers a free, no-obligation case evaluation and works on a contingency basis — there is no fee unless the claim is won. There is no financial risk in finding out whether a case qualifies.

A single missed deadline or incomplete medical file can set a claim back by months. Professional representation exists to remove that risk.

Contact Quikaid to start a free case evaluation

To see how a dedicated advocacy team can shorten the typical disability claims timeline, watch Why Partner with Quikaid.

Share via:

HIRE AMERICA'S DISABILITY EXPERTS NOW

If you need disability benefits, hire Quikaid now. You will not regret it. We will do everything possible to get your claim approved.

Sign our contract now online, complete our Free Case Evaluation, or call (800) 941-1321 so we can start the process of getting you approved for benefits! You have nothing to lose, and everything to gain.

The time to get started is NOW!